Mr McDermott sees managers of fixed income funds finding opportunities in subordinated European financials, emerging market debt and high-yield debt.

However, the next few years may prove more challenging for those relying on fixed income for their income needs, as Rathbones' fixed income managers Bryn Jones and Noelle Cazalis acknowledge.

“Arguably, income for fixed income managers is currently problematic, given government bond yields and credit yields have been suppressed by quantitative easing.

“However, there are some areas of value, in particular subordinated insurance and parts of the yield curve where you can benefit from roll down. This tends to be five to 12 years on the UK curve,” they explain.

Strategy challenges

Anthony Rayner, co-manager of the Miton Cautious Monthly Income fund, agrees fixed income managers will find it increasingly difficult to deliver their income targets.

“Over the past few decades, it has been relatively easy to generate an income and capital gain in fixed income because sovereign bond yields have been falling consistently, whereas equity strategies have been relatively volatile,” he says.

“Equity income has also been a good strategy, again, because of falling sovereign bond yields.”

He cautions: “As we move into an era of rising inflation it will be harder for both asset classes in the near term, but bond strategies are likely to be most challenged in the medium term."

Russ Mould, AJ Bell's investment director, points out there is a danger that as inflation expectations rise, they will "either drag bond yields with them or prompt a Bank of England interest rate increase, or both, potentially eroding the premium yield on offer from stocks".

He continues: "Equally, there is a risk dividends could be cut, especially as the FTSE 100’s dividend cover is thin by historic standards at around 1.6 times, when a two times cover ratio would be ideal.

"A bond-market blitz looks to be a bigger risk than dividend cuts at the moment, especially as only EasyJet, Pearson and Sainsbury's cut their shareholder payout in 2017 of late.

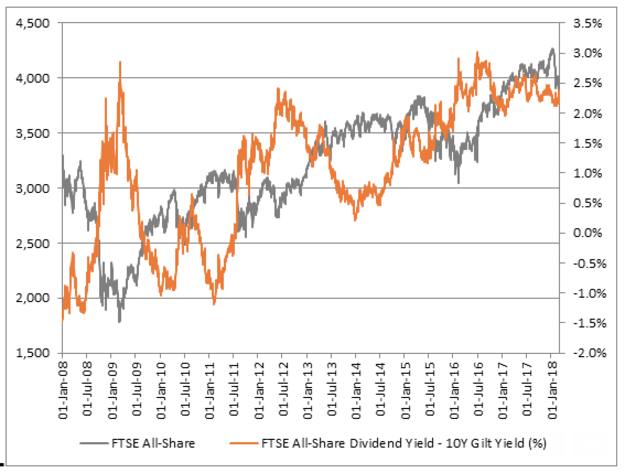

"But the 10-year UK gilt yield has come in from 1.64 per cent in mid-February to 1.5 per cent, and that retreat has helped the FTSE 100 by reaffirming stocks’ yield premium relative to bonds, even that comes in return for greater capital risk."

Source: AJ Bell/Thomson Reuters Datastream

Mr Rayner notes: “Within equity, we are finding income across geographies but particularly Europe ex UK, the UK and Asia. Within bonds, the majority of our income is generated from US and UK corporate bonds, which are very short dated.”

Ultimately, there will always be a need for income in client portfolios.

Carl Stick, manager of the Rathbone Income fund, believes: “The trends are as they have ever been, meaning as a strategy, the quest for dividend-paying shares may drift in and out of favour, as investors’ attitudes to risk waxes and wanes.