"There's no doubt more and more advisers see this kind of proposition as suitable for growing numbers of their own clients. These products can provide a very helpful foundation."

Standalone product

Importantly, according to Andrew Sajo, spokesman for The Source, the fact that lifestyle insurance is a standalone product makes it a good product for advisers to consider for clients.

He explains: "The vast majority of PPI was coupled with a financial services product, but short-term income protection plans are based on the customer's individual lifestyle commitments, rather than being coupled with a single product."

According to Mr Sajo, some 56 per cent of Source's IFAs and mortgage brokers said if you can get the product right, there is "huge potential" when it comes to providing short-term cover for clients.

He adds: "The main barriers to sale are the stigma attached to the PPI mis-selling, price and product flexibility. If you can tackle these barriers, this will give even more confidence to IFAs offering this type of product to clients."

Generation rent

For Emma Thomson, life office relationship director for Lifesearch, it is important to help more people get engaged with protection, and she believes specific products such as lifestyle insurance, given its short-term nature, can help a wide generation of people.

In particular, she points to Generation Rent as a prime market for short-term insurance products. With more people renting now than ever before, and a higher proportion of working people aged 40-plus living in rental accommodation, Ms Thomson believes a greater range of short-term, flexible insurance products are needed.

She explains: "Products designed for the rental market could really help. Too much emphasis is on protecting mortgages and there is not enough focus on renters, who are arguable more exposed in some cases.

"It would make sense to have a simple application process, so an automated acceptance-style product like PPI or accident, sickness and unemployment, could appeal better to consumers and advisers."

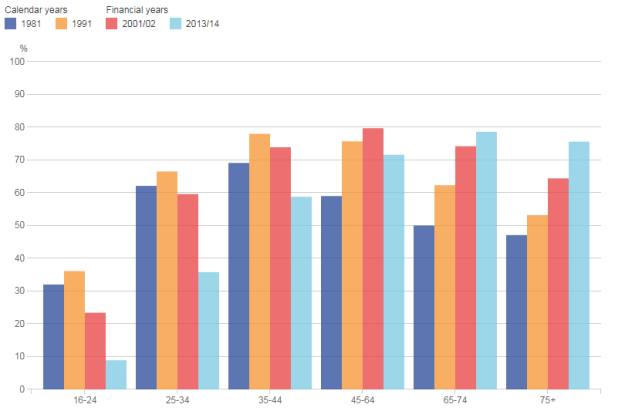

Indeed, figures from the Office for National Statistics show how since 2010, the number of homeowners aged 40 and under has fallen considerably. The pale blue bar shows just how much homeownership among the youngest - 18 to 24 - has fallen since the 1980s and 1990s.

Ms Thomson believes lifestyle insurance products go further than ASU, however, as ASU has exclusions for pre-existing conditions, which can be a downside. Another potential downside to ASU is that cover can be withdrawn or changed at the renewal stage.

Therefore, some form of shorter-term income protection plan like lifestyle insurance products, which would have an element of underwriting, would "make sense", she comments.

Engagement

Ms Thomson adds: "Moreover, short-term products can present the opportunity to get people engaged with protection quickly and easily, and use that as a stepping-stone to help arrange more comprehensive cover when they are ready for it."